Oil Shocks, Air Tragedies, and the Art of Staying Nimble

June 15, 2025•8 min read

Ever feel like you’re watching the same movie on repeat, except the plot twists keep getting wilder? That’s how markets have felt lately. Just when you think you’ve seen every possible surprise, the script flips again.

This week, the headlines served up a double feature: geopolitical drama and a very sobering tragedy, both with real consequences for investors.

So… grab your favourite drink… be it a double espresso, a grappa with water (no ice, naturally), or something equally fortifying and settle in. We’re about to unpack the week’s most important developments—and why staying nimble is more than just good advice… it’s essential for navigating this unpredictable market.

Recap: Where We Left Off (Week 23)

Last week, we saw the Trump-Musk feud rattle tech stocks, oil prices hold steady, and central banks keep everyone guessing. The mood was cautiously optimistic—but as always, the market was one headline away from a mood swing.

Markets are like brunch: just when you think you’ve got the menu figured out, someone orders the special and changes the whole vibe. Last week’s drama was a reminder that no matter how much you plan, the unexpected always finds a way to the table.

Oil Shocks, Air Tragedies, and Market Jitters

In This Week’s Edition:

- Israel-Iran tensions send oil prices soaring and markets into risk-off mode

- Air India Flight 171 crash shocks global aviation and raises safety concerns

- Fed holds steady, but markets anticipate two interest rate cuts before year-end

- Liquidity surges with U.S. M2 money supply hitting $22 trillion

- Private equity outlook: Why lower rates and more liquidity may boost exits

- Geopolitical risks & inflation: What they mean for your portfolio resilience

- Ed’s take: How to stay nimble when markets are messy—and what brunch can teach us about timing

US & Global Equities:

- S&P 500 and Nasdaq dipped sharply on Friday as tensions between Israel and Iran flared, with oil prices surging and investors flocking to safe havens.

- FTSE 100 and DAX (Germany) also retreated, though less dramatically, as European markets weighed the risk of a broader Middle East conflict.

- Bitcoin was volatile but ended the week flat—proving again that digital gold can be as unpredictable as a brunch guest who insists on ordering dessert first.

Macro & Policy:

- US Treasury yields edged higher as investors priced in the risk of sustained inflation from rising oil prices.

- Fed officials remained cautious, with the market now pricing in a September rate cut, though the path remains uncertain.

- China’s manufacturing PMI remained in contraction, but hopes for a tariff thaw helped sentiment.

- Europe & UK: The ECB and BoE are both in easing mode, but inflation and geopolitical risks are keeping policymakers cautious.

Economic Analysis

The Israel–Iran Attack

The week’s biggest shock came as Israel launched strikes on nuclear and military sites in Iran, sending oil prices soaring and stocks tumbling. Brent crude surged as much as 14% before settling up 7% for the week, while WTI crude followed suit. The immediate market reaction was a flight to safety: equities fell across Asia, Europe, and the US.

Market Impact:

- Oil prices: The spike in oil prices is expected to feed through to inflation, with the IMF estimating that every 10% rise in oil prices adds about 0.4 percentage points to inflation in advanced economies.

- Shipping and trade: Insurance premiums for shipping in the region have risen, and any disruption to key waterways could further strain global supply chains.

- Growth outlook: The risk of a wider conflict has added uncertainty to an already fragile global growth environment, with potential knock-on effects for business investment and consumer confidence.

With inflationary pressure increasing the likelihood of interest rate dropping declines and this will lead to constrained risk asset growth. (see the interest rate piece below).

The Israel-Iran attack feels like a brunch guest spilling red wine on the tablecloth; sudden, messy, and impossible to ignore. Markets hate surprises, especially when they come with a side of oil inflation. The lesson? Always keep a napkin (or a hedge) handy.

The Air India Crash

The tragic crash of Air India Flight 171 has sent shockwaves through the aviation industry and the broader Indian economy. The disaster, which claimed over 200 lives, is the deadliest civil aviation accident in India this decade and the first fatal hull loss for the Boeing 787.

On behalf of the Beaufort Society, I would like to express my deepest sympathies to all those affected by this terrible tragedy. Our thoughts are with the families, friends, and colleagues of the victims.

Market & Sector Impact:

- Airline and aerospace stocks: Boeing and Air India shares fell sharply, and the incident has raised fresh concerns about safety, maintenance, and the challenges facing India’s rapidly growing aviation sector.

- Industry challenges: The crash comes at a time when Indian airlines are already grappling with grounded planes, engine failures, and labour disputes. The Tata Group’s ambitious plans to modernize Air India now face renewed scrutiny.

- Broader implications: The tragedy underscores the fragility of India’s aviation boom and the importance of operational discipline, safety culture, and financial resilience in a high-growth, high-risk environment.

The Air India crash is a sobering reminder that even the most ambitious growth stories can be derailed by a single moment of tragedy. In markets and in life, it’s not just about how fast you grow. It’s about how well you manage risk along the way.

Weekly Market Table

What’s Pertinent This Week?

- Central Bank Watch: The Fed, ECB, and BoE are all in easing mode, but geopolitical and inflation risks are keeping policymakers cautious. No interest rate reductions for the FOMC next week.

- Oil Shock: The Israel-Iran attack has reignited fears of sustained inflation and slower growth, with oil prices surging and shipping costs rising.

- Aviation Tragedy: The Air India crash has shaken confidence in the sector and highlighted the challenges of managing rapid growth in a high-risk industry.

- Global Growth: China’s manufacturing PMI remains weak, but hopes for a tariff thaw are keeping sentiment from souring further. Europe and the UK are showing slow but positive momentum.

This week was a reminder that markets are as much about psychology as they are about fundamentals. The Israel-Iran attack and the Air India crash were like two uninvited guests at brunch…. sudden, disruptive, and impossible to ignore.

The key takeaway? Keep your portfolio balanced and your sense of humour intact.

Private Equity’s Macro Insights

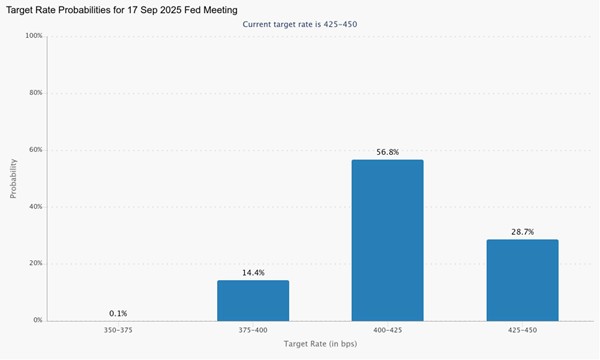

Interest Rates and Monetary Policy: The Summer Forecast

Interest rates are beginning to drop. The U.S. Federal Reserve, having held rates steady at 4.25–4.50%, now foresees two cuts by year-end, potentially bringing the target range down to 3.75–4.00%. The European Central Bank and Bank of England are also in easing mode, citing inflation under control and a cautiously optimistic outlook for growth. Below is a chart showing the post summer interest rate probabilities.

This marks a clear pivot from restrictive to neutral or even accommodative policy, as central banks seek to avoid a sudden cooling of the labour market and keep the economy on track.

For private equity, lower rates mean cheaper financing for buyers, higher valuations, and a more receptive environment for exits; especially IPOs and mergers.

Over the next three weeks, we will take a deeper educational dive into the mechanics of interest rates and their impact on private equity exits. Expect practical insights, real-world examples, and actionable strategies for navigating the evolving rate environment.

Monetary Liquidity – The Hidden Tailwind

Monetary policy and liquidity conditions have already moved favourably. The U.S. M2 money supply has climbed to a record $22 trillion in April 2025, signalling the end of tightening and a return to monetary expansion. While this liquidity surge hasn’t yet fully trickled through to the real economy or deal pipelines, it’s a powerful tailwind for market sentiment and, eventually, for exit activity.

As quantitative tightening concludes, idle liquidity is expected to decrease, potentially pushing generic money market rates higher and creating a more natural environment for risk assets. For private equity, this means more capital chasing deals, higher valuations, and a smoother path to exits.

This summer, we will also explore the concept of monetary liquidity in greater depth, examining how shifts in central bank policy and money supply affect deal-making, valuations, and exit strategies. Stay tuned for a series of educational pieces that will help you understand and leverage these macro forces in your portfolio.

Exits are like brunch: timing is everything. You don’t want to be the last one at the table when the coffee runs out. With interest rates dropping, liquidity on the rise, and central banks in easing mode, we may be on the cusp of a more favourable exit environment—even if the full effect hasn’t yet reached Main Street. For the nimble and prepared, this could be the moment to start lining up those exit plans, ready to move when the market’s appetite returns.

Ed’s Final Word

Week 24 reminded us that markets are never dull, especially when geopolitics, tragedy, and monetary policy collide.

For investors: stay nimble, stay diversified, and don’t be afraid to add a splash of grappa (or a hedge) to your portfolio.

As always, these are the thoughts and opinions of mine and no one else’s—not even Beaufort Private Equity Limited. Please do your own research before making investment decisions and reach out to your Beaufort relationship manager if you have any queries or follow-ups.

Further Reading:

- CNN Fear & Greed Index (Live)

- Reuters – Israel–Iran Attack

- CNBC – Oil Prices Jump and Stocks Drop

- Reuters – Air India Crash

- Economic Times – India’s Aviation Boom

#MarketInsights#Week24Update#OilPrices#GeopoliticalRisk#IsraelIranConflict#AviationSector#PrivateEquity#ExitStrategy

– Practicing Chartered Accountant; experienced (25+ years) finance professional for regulated financial services organisations – Director and co-owner of Gibraltar FSC regulated Company & Trust Management Company – Strong financial modelling and financial planning and analysis for FTSE listed financial conglomerate – Treasurer (£1BN of AUM and £250M of regulatory capital) for regulated financial services organisation – Board experienced (both Group and subsidiary) along with leadership chairing committees – Experienced at running large multi located departments and teams – Corporate Finance experience in both technology, private equity and banking M&A – International audit experience UK GAAP, US GAAP, IFRS and Gibraltar GAAP – Strong managerial finance, financial accounting and financial internal control including Sarbanes Oxley audits – ERP implementation experience in Oracle and NetSuite and online accounting systems – Big 4 ACA qualification with treasury, finance, corporate finance and consultancy experience – Cambridge university education