Liquidity, Listings & the September Pivot: What Investors Need to Know Now

June 22, 2025•11 min read

If you’ve ever watched a tightrope walker, you know the trick isn’t just about balance … it’s about knowing when to shift your weight, when to pause, and when to take the next step. That’s a bit like this week’s markets: oil prices settled, tech stocks bounced, and the world kept spinning; sometimes a little too fast for comfort. So grab your drink of choice (double espresso, grappa, or something with a little more kick), and let’s unpack another week of twists, turns, and the occasional plot twist.

Recap: Where We Left Off (Week 24)

Week 24: Oil Shocks, Air Tragedies, and the Art of Staying Nimble

Last week, we saw oil prices spike, stocks wobble, and the world reminded that even the best-laid plans can be upended by a single headline. The Israel-Iran conflict and the Air India tragedy were stark reminders that risk and resilience go hand in hand. Meanwhile, central banks kept their hands steady on the tiller, and private equity exits looked a little brighter as interest rates edged lower and liquidity crept back into the system.

Markets are like a Sunday brunch: just when you think you’ve got the menu figured out, someone orders the special and changes the whole vibe. Last week was a reminder that no matter how much you plan, the unexpected always finds a way to the table.

This Week: Settling Dust and Shifting Sands

US & Global Equities:

- S&P 500 and Nasdaq bounced back after last week’s oil shock, with tech leading the charge as investors looked past geopolitical noise and focused on earnings and central bank signals.

- FTSE 100 and DAX (Germany) were steadier, with European markets taking their cues from a calmer oil market and hints of further easing from the ECB.

- Bitcoin held near recent highs, proving once again that digital assets can be as unpredictable as a brunch guest who insists on ordering dessert first.

Macro & Policy:

- US Treasury yields stabilized as oil prices retreated and inflation fears eased, at least for now.

- Fed officials reiterated a cautious stance, but the market is still pricing in a September rate cut, with a growing sense that the worst of the inflation scare is behind us.

- China’s manufacturing PMI remained in contraction, but hopes for a tariff thaw kept sentiment from souring further.

- Europe & UK: The ECB and BoE are both in easing mode, with inflation and geopolitical risks keeping policymakers cautious but not panicked.

Sometimes, the most important thing you can do is take a step back and let the dust settle. This week, markets did just that, and in doing so, reminded us that resilience is as much about patience as it is about action.

Economic Analysis: The Week That Was

After the turbulence of Week 24, markets took a breath. Oil prices settled back below $80 a barrel, easing fears of sustained inflation and giving central banks a little more room to manoeuvre. The Israel-Iran standoff remains tense, but for now, the risk of a wider conflict has receded …. at least in the eyes of the market.

Meanwhile, the Air India tragedy continues to cast a shadow over the aviation sector, with safety and operational discipline under renewed scrutiny. For investors, it’s a reminder that growth and risk are two sides of the same coin, especially in industries where safety and reliability are non-negotiable.

If you ever doubted that markets are as much about psychology as they are about fundamentals, this week should put that to rest. The Israel-Iran attack and the Air India crash were like two uninvited guests at brunch … sudden, disruptive, and impossible to ignore. The key takeaway? Keep your portfolio balanced and your sense of humour intact.

Weekly Market Table

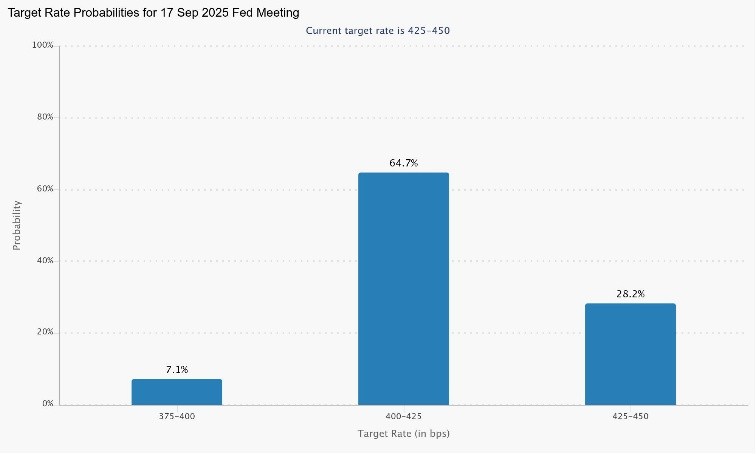

Note: The “Fed Rate Cut Prob. (Sep 17)” row reflects the market-implied probability of the Federal Reserve cutting interest rates at its September 17, 2025, meeting, based on the latest futures pricing. This week, the probability stands at approximately 64%, up from about 58% last week, signalling increased market expectations for policy easing. Please see the section on interest rates below.

What’s Pertinent This Week?

- Oil Shock Fades: Oil prices retreated, easing inflation fears and giving central banks a little more room to manoeuvre.

- Tech Bounce: Tech stocks led the market higher as investors looked past geopolitical noise and focused on earnings and central bank signals.

- Gold Steady: Gold continued to hold near record highs, reflecting ongoing demand for safe-haven assets amid lingering uncertainty.

- Central Bank Watch: The Fed, ECB, and BoE are all in easing mode, with inflation and geopolitical risks keeping policymakers cautious but not panicked.

- Global Growth: China’s manufacturing PMI remains weak, but hopes for a tariff thaw are keeping sentiment from souring further. Europe and the UK are showing slow but positive momentum.

This week was a reminder that markets, like life, are about momentum and patience. Sometimes the best move is to let the dust settle and wait for the next opportunity to present itself. The key takeaway? Stay nimble, stay diversified, and don’t be afraid to pivot when the moment calls for it.

Private Equity’s Macro Insights:

The Liquidity Wave: Digital, Regulatory, and the “Picks and Shovels” Play

Last week, we began our deeper dive into monetary liquidity and its impact on private equity exits. This week, we’ll take a closer look at how digital liquidity, fuelled by recent listings and regulatory changes, is reshaping the landscape.

Disclosure: I participated in Circle’s IPO. In the following paragraphs, I detail my personal motivations for this decision and present some of my research into this asset class.

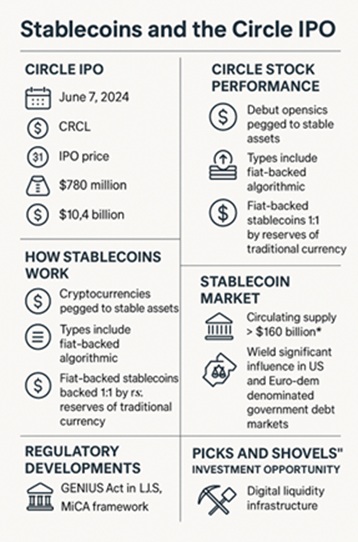

Circle’s IPO: A New Era for Digital Liquidity

Circle, the stablecoin giant behind USDC, made headlines with its $1.05 billion IPO on the New York Stock Exchange. Shares debuted at $31, surged as high as $248, and closed the week near $240 … a stunning debut that underscored the market’s appetite for digital assets and the infrastructure that powers them. Circle’s success is more than just a win for crypto: it’s a sign that digital liquidity is becoming mainstream, and that investors are willing to bet big on the “picks and shovels” of the digital economy.

How Stablecoins Work

Stablecoins are digital tokens designed to maintain a stable value by pegging to a reference asset; most commonly the US dollar (a fiat currency, meaning government-issued money not backed by a physical commodity like gold). They come in several forms: fiat-backed (like USDC and USDT), commodity-backed, crypto-collateralized, and algorithmic. Fiat-backed stablecoins, the most widely used, are backed by reserves of cash and short-term government securities, ensuring that each token can be redeemed for its face value. This stability makes stablecoins a vital bridge between traditional finance and the digital economy, enabling fast, low-cost, and transparent transactions across borders and platforms.

How Circle Makes Money from USDC

Circle’s business model is elegantly simple. When users want USDC, they send Circle real dollars. Circle takes those dollars and mints new USDC tokens in exchange, while simultaneously depositing the dollars into segregated reserve accounts holding mostly short-term U.S. Treasury bills and cash. When users want to cash out, the process reverses: Circle redeems USDC tokens, destroys them, and returns the equivalent dollars from reserves.

The Profitability Cycle: Circle, Interest Rates, and a Counterbalance to Risk Assets

Circle’s profitability is directly tied to short-term interest rates. The company earns interest on the reserves backing USDC; primarily short-term Treasuries and cash. In a high-rate environment, this “float” generates substantial revenue: with nearly $60 billion in circulating USDC and reserves earning around 5% interest, Circle can generate billions in gross interest income annually. After sharing some of this income with partners (notably Coinbase) and covering operational costs, Circle keeps a significant portion as net revenue.

This makes Circle’s business a leveraged play on short-term rates. When rates are high, Circle’s profits surge; when rates fall, so does its income. This cyclicality gives Circle a unique profile: its fortunes rise as risk assets (like equities and crypto) often come under pressure from higher rates, and vice versa. In this way, Circle and stablecoins can act as a counterbalance to traditional risk assets; providing a stable, yield-generating anchor in portfolios when other markets are volatile.

The Size of the Market and Its Growing Influence

The stablecoin market is now a major force in global finance. As of mid-2025, over $160 billion in stablecoins are in circulation, with USDC accounting for nearly $60 billion of that total. The largest stablecoin, Tether (USDT), has a market cap of over $150 billion. Together, these digital dollars are not just a niche product … they are a new class of financial instrument, reshaping how money moves around the world.

Stablecoins are also becoming a major buyer of short-term government debt. With billions parked in Treasury bills and other high-quality liquid assets, stablecoin issuers like Circle are providing vital liquidity to governments, helping to fund public spending and smooth out market volatility. This growing influence means that stablecoins are now a key part of the global financial plumbing, with the potential to impact everything from interest rates to the availability of credit.

Recent Regulatory Developments

The regulatory landscape for stablecoins is rapidly evolving. In June 2025, the US Senate passed the GENIUS Act, a landmark bill establishing a federal regulatory framework for stablecoins. The Act requires issuers to hold reserves of high-quality, liquid assets, conduct monthly audits, and comply with anti-money laundering (AML) and consumer protection standards. If enacted, this will provide much-needed clarity and stability for the sector, boosting confidence among investors and users.

In the EU, the Markets in Crypto-Assets (MiCA) regulation is reshaping the stablecoin market by imposing strict transparency, reserve, and licensing requirements. This has led to the delisting of non-compliant tokens from major exchanges and a shift of liquidity toward regulated alternatives.

The “Picks and Shovels” Opportunity

With the rise of stablecoins and the increasing importance of digital liquidity, private equity and long-term investors are focusing on the infrastructure that enables this transformation: exchanges, custodians, payment rails, and regulated stablecoin issuers. As regulatory clarity improves and institutional adoption grows, these “picks and shovels” investments are becoming a cornerstone of digital asset portfolios.

Sometimes, the best way to play a trend is to invest in the infrastructure that makes it possible. In the world of digital liquidity, that means betting on the platforms and services that enable the flow of capital and not just the assets themselves.

As the Circle IPO and the GENIUS Act show, the future of liquidity is digital, regulated, and full of opportunity for those who know where to look.

Interest Rate Outlook for September: What It Means for Private Equity

This week, I have added the market-implied probability of a Fed rate cut at the September 17 FOMC meeting to our Weekly Market Table. As of now, futures markets are pricing in a roughly 64% chance of a rate reduction at that meeting, up from about 58% last week. This reflects growing market confidence that the Fed will shift from its current “higher for longer” stance toward a more accommodative policy, as inflation pressures ease and economic growth shows signs of moderation.

For private equity, the potential for a September rate cut is highly significant. Lower interest rates reduce the cost of borrowing, making it cheaper for funds to finance new deals and for portfolio companies to refinance existing debt. This can boost deal activity, increase valuations, and make exit strategies, such as IPOs and trade sales; more attractive. At the same time, a more accommodative monetary policy can increase competition for deals, as more capital enters the market seeking yield, potentially leading to higher purchase prices and tighter margins.

However, the prospect of lower rates also brings risks. Increased competition can drive up asset prices and lead to overvaluation, while the availability of cheap debt can encourage excessive leverage. For private equity managers, the key will be to remain disciplined, focusing on operational improvements and value creation rather than relying solely on financial engineering.

Ed’s Final Word

Week 25 was a reminder that markets, like life, are about momentum and patience. Sometimes the best move is to let the dust settle and wait for the next opportunity to present itself. For private equity and risk asset investors, the lesson is clear: stay nimble, stay diversified, and don’t be afraid to pivot when the moment calls for it.

As always, these are the thoughts and opinions of mine and no one else’s … not even Beaufort Private Equity Limited. Please do your own research before making investment decisions and reach out to your Beaufort relationship manager if you have any queries or follow-ups.

Further Reading:

- CNN Fear & Greed Index (Live)

- Reuters – Circle’s Blockbuster IPO

- CNBC – Circle Soars in NYSE Debut

- Digital Asset Regulation and The CLARITY Act of 2025

- Business Wire – Circle IPO Pricing

- Investor’s Business Daily – Cathie Wood and Circle

Week 25, 2025: In markets, the only constant is change … so keep your wits, your watchlist, and your breakfast close at hand. And if you’re feeling adventurous, try that double espresso with a splash of grappa. You might just like it.

#PrivateEquity#CircleIPO#DigitalLiquidity#Stablecoins#InterestRates#MonetaryPolicy#MarketInsights#Macroeconomics#FinancialMarkets#beaufortprivateequity

– Practicing Chartered Accountant; experienced (25+ years) finance professional for regulated financial services organisations – Director and co-owner of Gibraltar FSC regulated Company & Trust Management Company – Strong financial modelling and financial planning and analysis for FTSE listed financial conglomerate – Treasurer (£1BN of AUM and £250M of regulatory capital) for regulated financial services organisation – Board experienced (both Group and subsidiary) along with leadership chairing committees – Experienced at running large multi located departments and teams – Corporate Finance experience in both technology, private equity and banking M&A – International audit experience UK GAAP, US GAAP, IFRS and Gibraltar GAAP – Strong managerial finance, financial accounting and financial internal control including Sarbanes Oxley audits – ERP implementation experience in Oracle and NetSuite and online accounting systems – Big 4 ACA qualification with treasury, finance, corporate finance and consultancy experience – Cambridge university education